By BRIAN KLEPPER and JEFFREY HOGAN

GoodRx’s planned initial public offering recently made the news, notable because the company, launched in 2011, has been profitable since 2016. Evidently, it’s become unfashionable for investors to demand proof of performance, so GoodRx’s results shone like a beacon. By contrast, most health care firms seeking funding convey bold aspirations and earnest promises. Investors throw in with them and hope for the best.

But few new entrants seem to do the necessary advanced due diligence to assess exactly where and how their product, service or innovation should be positioned in the health care ecosystem to derive maximum value. Ironically, COVID has intensified and highlighted the fragility of the health care ecosystem, as well as the greater disruption opportunities available to new entrants.

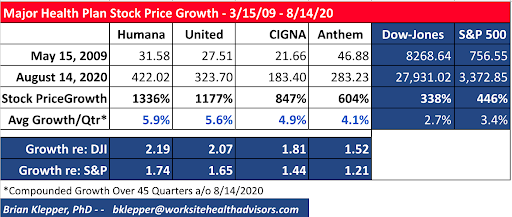

Health care has become irresistible to investors, the outgrowth of the industry’s dominant players’ spectacular financial performance. Over the past 45 quarters, for example, major health plan stock prices have grown 4-6 percent per quarter, 1.2-2.2 times the growth rates of DJI and S&P (See the table below). Investors hope to either 1) capitalize on the health care’s ongoing culture of overtreatment and egregious pricing, or 2) support and share in the savings associated with rightsizing care and cost.

The result has been a torrent of investment. Mercom Capital reports that, in the last decade, investors have poured $ 50 billion into some 5,000 digital health startups, each one no doubt guaranteeing wholesale health system disruption that never arrived.

There are a couple of messages here. In the main, few health care startups are constituted to thrive. And apparently, few investors critically evaluate a venture’s broader design elements to gauge its chances for success. Many startups have great ideas and some even operationally execute those ideas well, but gaining traction in the health care marketplace requires much more than that. A viable venture must also integrate with its clients’ workflows, and connect with existing players in the larger health care management ecosystem.

There’s a huge opportunity to disrupt the status quo, but it requires a thoughtful, comprehensive design. As Michael Porter pointed out, “If all you’re trying to do is essentially the same thing as your rivals, then it’s unlikely that you’ll be very successful.”

Purchasers of health care risk management services – e.g., employers, worksite clinic firms, captive insurance arrangements, stop loss carriers, provider risk managers – exist in a high noise-to-signal environment and are constantly besieged by vendors. If they are value-focused, the question is whether the venture can quickly differentiate by demonstrating consistently superior results, meaning better health outcomes and/or lower costs than usual approaches. Assuming they can do that, there are more hurdles to clear to have a shot. For example:

- Is the venture aimed at the right audience? If the venture achieves lower costs with equal or better outcomes, it may be wholly uninteresting to health plans that are still volume-based, that make more if health care costs more. Lower costs here likely translate to lower net revenues, earnings, stock price and market cap, results that health plans may avoid at all costs. But value-focused purchasers may be inclined to take notice.

- Potential clients want to know about other clients’ experience. Are there testimonials from people you can talk with, attesting to a program’s operational excellence and vendor-client warmth?

- Can the program scale, delivering consistent results independent of geographic location or the population’s demographics?

- Are the services sticky, remaining effective over time? Can they provide ongoing, predictable management of clinical or financial risk?

- Can clients come quickly up to speed on the services? Does the vendor provide training that facilitates ease of use with the program?

- Are all key constituencies aware of the program. If a physician-based program improves health outcomes and reduces cost, are provider risk managers aware of it and demanding its use?

- Do the processes integrate seamlessly into the clients’ existing workflows? If, for example, a new physician tool is on a different platform than the electronic health record, it may require unaffordable additional steps and will almost certainly fail.

- Does the program exchange information easily with other critical management vendors? Is it mindful that it must fit into a broader existing management structure?

- Is the vendor willing to financially guarantee the achievement of performance targets? Doing so puts its money where their mouth is, conveying confidence in its ability to deliver.

Some well-funded ventures have used marketing bluster to successfully convince the market that they’re excellent – see Al Lewis’ scathing review of Livongo – but in a health care market that increasingly considers value, purchasers are becoming more discriminating. In addition to performance data, many want to see independent, third party validation, like that provided by The Validation Institute, affirming that the approach in question works.

Livongo and others are going directly to employers with their services, and desperate employers seem ready to listen. Other unique direct disruptors like Vera Whole Health and Integrated Musculoskeletal Care offer employers bonafide, at-risk solutions that supplant existing fee-for-service provider payment methods. They often use hybrid models that take responsibility for specific patients, and extend in-person and virtual primary care with the full functionality of advanced primary care. This agnostic model can steer to warranted episodes-of-care bundles for the biggest programmatic spend drivers.

True innovation is exploding now, if you can spot the right firms. Companies like Dispatch Health are offering a quality at home urgent care solution that threatens brick and mortar urgent care. MediSync’s artificial intelligence-driven tool suite is revolutionizing chronic care management, which represents 75 percent of health care spend. ConferMed offers a national virtual specialty network that improves outcomes and drives out unnecessary care and cost.

Employers and at-risk organizations are increasingly abandoning traditional fee-for-service health care models in favor of value-based solutions, with payment systems that demand accountability and predictability. New ventures have a huge opportunity to succeed, but only if they have appropriately interpreted all of their opportunities in this new landscape. Most have not.

Brian Klepper is a health care analyst and Principal of Worksite Health Advisors, in Charlotte, NC.

Jeffrey Hogan is a health benefits advisor and Principal of Upside Health Advisors in Farmington, CT.

Spread the love